Assets are resources a company owns that have an economic value. Assets are represented on the balance sheet financial statement. Some common examples of assets are cash, accounts receivable, inventory, supplies, prepaid expenses, notes receivable, equipment, buildings, machinery, and land. Assets are resources a business owns that have an economic value. Some commonexamples of assets are cash, accounts receivable, inventory,supplies, prepaid expenses, notes receivable, equipment, buildings,machinery, and land. The expanded accounting equation is a form of the basic accounting equation that includes the distinct components of owner’s equity, such as dividends, shareholder capital, revenue, and expenses.

How to use the Expanded Accounting Equation

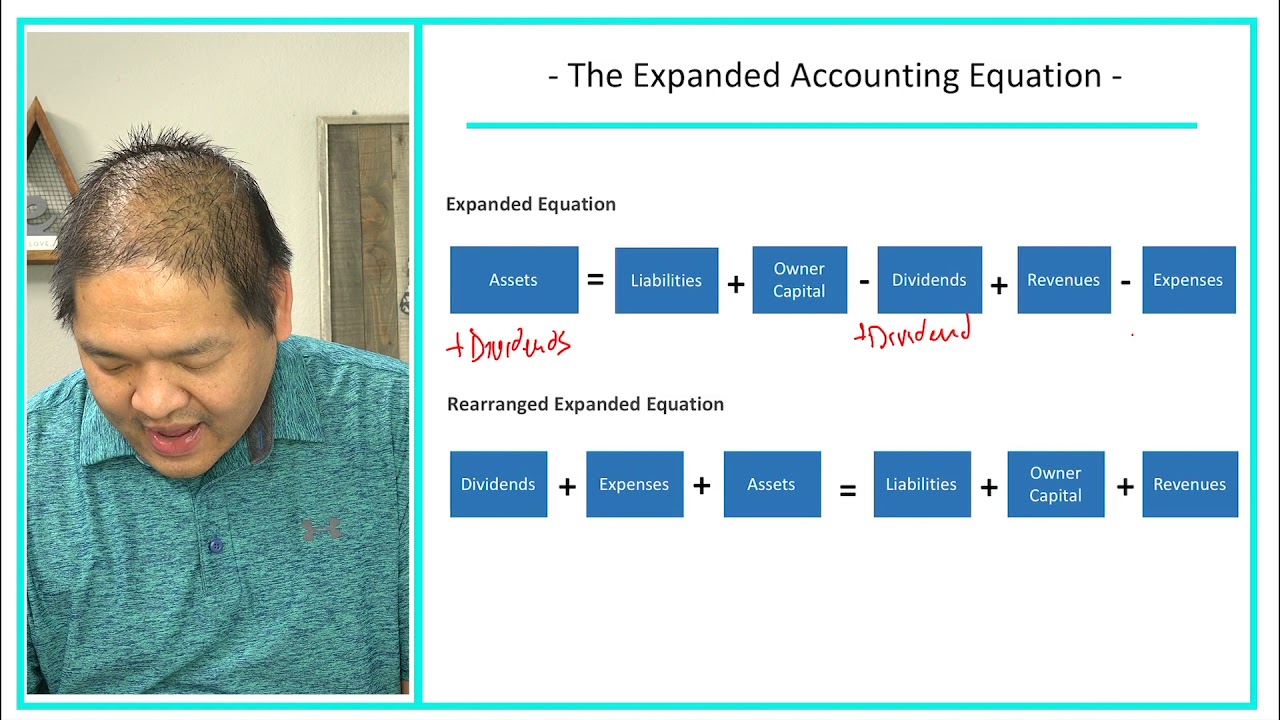

To understand the expanded accounting equation, knowing the key components is critical. Substituting for the appropriate terms of the expanded accounting equation, these figures add up to the total declared assets for Apple, Inc., which are worth $329,840 million U.S. dollars. I hope I was able to explain to you what the expanded accounting equation means, give you good examples, show you how it is calculated, and why it’s important.

Explaining Assets, Liabilities, and Equity in an Expanded Accounting Equation

By breaking down owner equity into revenue and expense components, bookkeepers can report more specific information about where that equity comes from, and what is causing it to ebb and flow. An analysis of a company’s income statement is a key goal behind use of the expanded accounting equation, as it provides a better understanding of profit trends. As seen in the example above, the net result how does the tax exclusion for employer of the expanded accounting equation is such that the corporation’s assets are equal to the net impact of stockholder equity, liabilities, and net earnings. A balanced equation also ensures that the whole accounting process has been followed properly. It further helps strengthen the fact that all the debit and credit entries about all transactions entered during the period have been considered.

- Machinery and buildings are often called PPE – Property Plant and Equipment.

- Therefore, always consult with accounting and tax professionals for assistance with your specific circumstances.

- The Basic Accounting Equation should typically be your go-to formula for broadly assessing your company’s finances.

- This means that the expenses exceeded the revenues forthe period, thus decreasing retained earnings.

Expanded Accounting Equation: Definition, Formula, How It Works

The expanded equation is used to compare a company’s assets with greater granularity than provided by the basic equation. You will notice that shareholders’ equity increases as new shares in the business are issued and as revenues grow; and decreases from dividend payouts and expenses. Shareholders’ equity is reported on the balance sheet in the form of share equity and retained earnings.

This may be difficult to understand where these changes have occurred without revenue recognized individually in this expanded equation. This expansion of the equity section allows a business to see the impact to equity from changes to revenues and expenses, and to owner investments and payouts. This may be difficult to understand where these changes have occurred without revenue recognised individually in this expanded equation. It is important to have more detailin this equity category to understand the effect on financialstatements from period to period.

The normal balance for the equity category is a credit balance whereas the normal balance for dividends is a debit balance resulting in dividends reducing total equity. The owner’s investments in the business typically come in the form of common stock and are called contributed capital. There is a hybrid owner’s investment labeled as preferred stock that is a combination of debt and equity (a concept covered in more advanced accounting courses).

Understanding the expanded accounting equation can be instrumental for any business owner. It assists in translating complex financial transactions into simple, digestible insights that can inform strategic decision-making. Withdrawing refers to the ‘Draws’ component in the expanded accounting equation. In this context, withdrawal means the owner’s removal of assets (cash or otherwise) from the business for personal use. Machinery is usually specific to a manufacturing company that has a factory producing goods. The accounts are presented in the chart of accounts in the order in which they appear on the financial statements, beginning with the balance sheet accounts and then the income statement accounts.

Another unique aspect of this particular equation is the component entitled “owner’s draws.” This refers to an owner’s ability to withdraw funds from a company, usually to pay salaries (including his or her own). This occurs most often in what is called a limited liability company, in which the owner is also the shareholder and no outside creditors are involved. In the case of stockholder equity, the draws to cover salaries take the form of dividends paid out by investors. The expanded equation highlights where and how these draws decrease overall equity.